To A/B, or Not To A/B, That is the Question

Posted on: August 10, 2023

Botti & Morison Estate Planning Attorneys, Ltd.

Most revocable living trusts for married couples, established prior to 2018, require that the trust be divided into two or more “sub-trusts” upon the death of the first spouse. This is for federal estate tax or “death tax” planning purposes. These trusts are known as A/B or A/B/C Trusts. They were designed primarily to reduce or eliminate estate taxes by preserving the federal estate tax exemption (the value of assets which can pass free of tax) of the first to die.

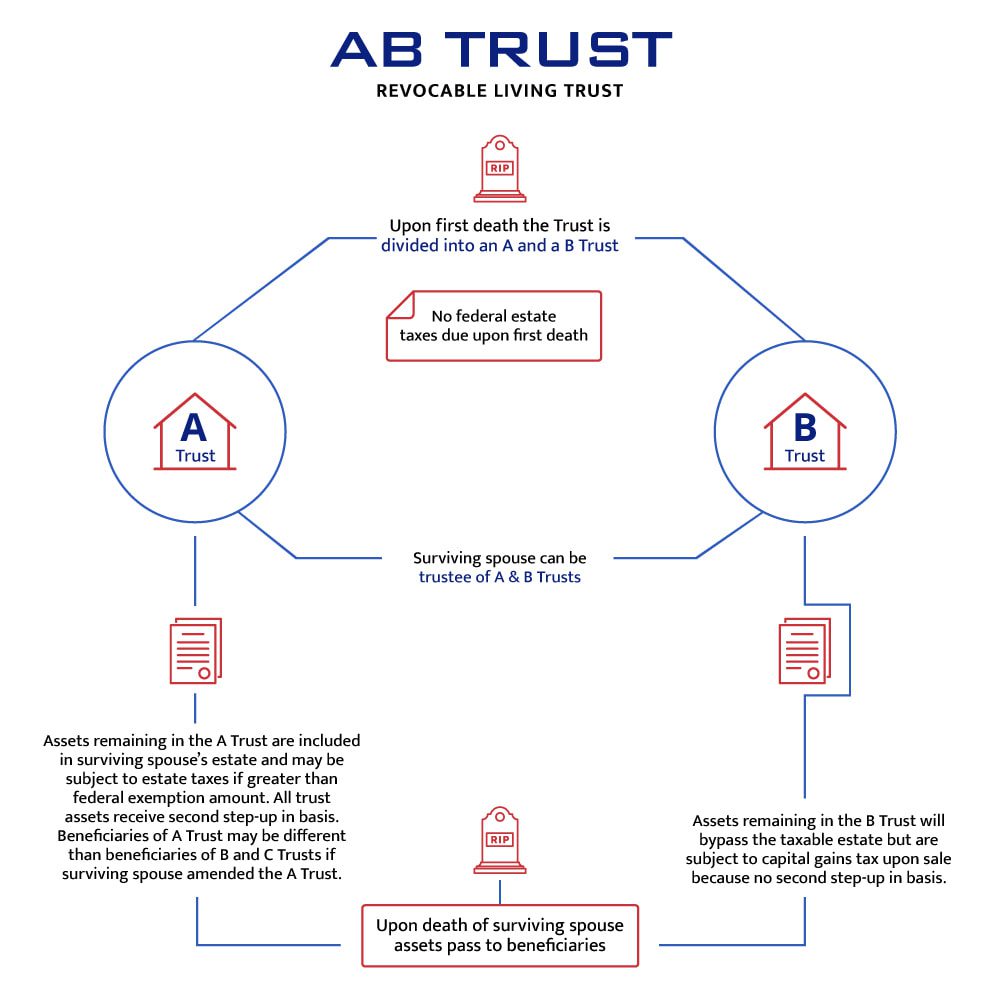

An A/B Trust works like this: Upon the death of the first spouse the B Trust is funded with the first to die’s assets (one half of their community property and all of their separate property) up to the applicable federal estate tax exemption amount. The exemption acts as a cap. Any excess assets of the first to die beyond the exemption, along with all of the assets owned by the surviving spouse, are allocated to the A Trust.

The A Trust assets are included in the surviving spouse’s estate for federal taxation purposes. This does not mean taxes will be automatically owed. There will be zero taxes owed as long as the surviving spouse’s taxable estate is below the federal estate tax exemption at the time of their death (currently $12.92 million). These assets also get an additional cost basis adjustment (known as the “second step-up in basis”) at the surviving spouse’s death. This results in potentially significant tax savings upon sale. Although the B Trust avoids federal estate tax, assets held in this trust do not receive a basis adjustment upon the death of the surviving spouse. However, the future growth of these assets remains outside the gross estate of the surviving spouse at their death.

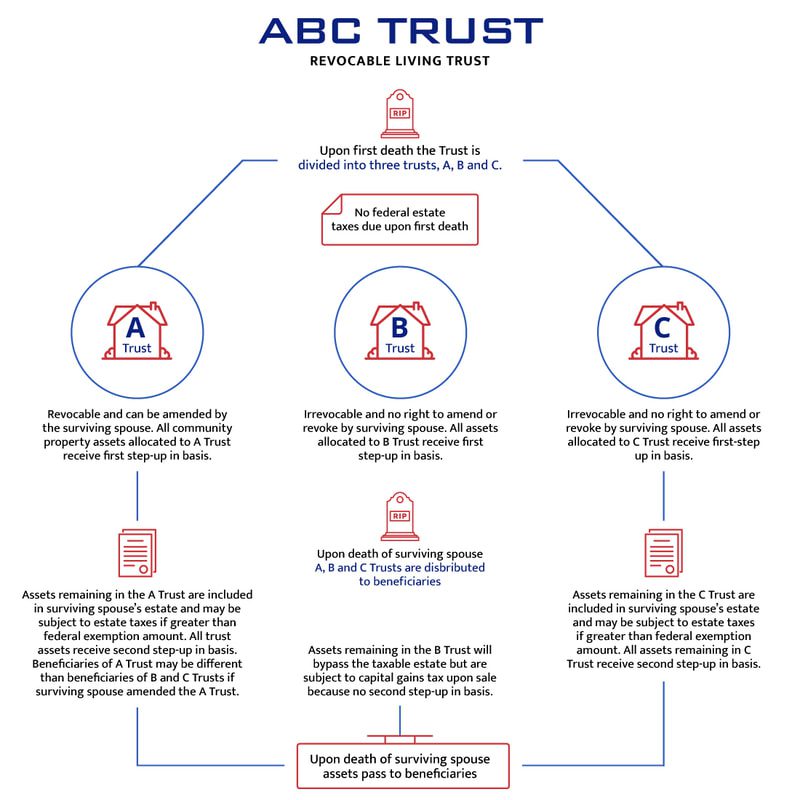

An A/B/C Trust is similar to an A/B Trust. It is used in larger estates when the first to die’s assets are greater than their federal estate tax exemption. The excess assets of the first to die, above their exemption amount, are allocated to C Trust. There is no tax on the first death because C Trust is funded by using the “unlimited marital deduction.” However, assets allocated to C Trust and A Trust may face estate tax on the death of the surviving spouse if they exceed the surviving spouse’s estate tax exemption.

B Trust and C Trust will each usually be required to file their own income tax returns. The net income of these trusts generally is payable to the survivor and passes through to the survivor for income tax purposes. The B Trust and C Trusts can have limits and restrictions on the availability of principal for the survivor. Both the A Trust and the C Trust assets will receive second basis adjustment when the surviving spouse dies. The B Trust will not.

Since the estate tax exemption prior to 2018 was much less than now, these A/B or A/B/C Trusts were prudent for many middle-income families. They made economic sense because the administrative burden of having an A/B or A/B/C Trust paled in comparison to the possibility of having assets in excess of the federal estate tax exemption which is taxed at a rate as high as fifty-five percent (55%).

The new tax law, effective in 2018, increased the federal estate tax exemption dramatically. The 2023 exemption is $12.92 million for individuals and $25.84 million for married couples. As a result, the overwhelming majority of people have estates that are far below the $12.92 million exemption thereby eliminating the need for federal estate tax planning with the use of A/B or A/B/C Trusts. Married couples can maintain one trust until the second spouse dies without the need for any sub-trust division on the first death. This type of joint trust is called a non A/B Trust and is by far easier and less costly to administer.

Here are the cons of an A/B or A/B/C Trust:

1. It costs money and is more complicated. Significant legal and accounting fees may be required to implement the mandatory A/B or A/B/C Trust split. The total date of death value of all assets must be obtained. Real estate and business interests must be appraised. Once the sub-trust division has occurred, the surviving spouse will be required to file a separate tax return for each sub-trust on a go forward basis, in addition to their own personal tax return.

2. Lack of Privacy. California law requires that the beneficiaries of the B or B/C Trusts are entitled to notification and a copy of the relevant portions of the trust document within 60 days from the date of the death of the first spouse. Moreover, these beneficiaries have legal rights that enable them to receive accountings of the trust assets. They also can drag the surviving spouse into court by petitioning the probate court in the event that they believe the surviving spouse did not properly fund and/or administer the B or B/C Trusts. Surviving spouses often begrudge that beneficiaries have these rights.

3. Irrevocability. The surviving spouse’s control over the sub-trust assets usually is limited because the B Trust or the B/C Trusts are irrevocable and can only be changed by the surviving spouse by seeking court intervention. This can come at great expense and uncertainty. There are plenty of valid reasons why a surviving spouse may want to amend their estate plan to account for changed circumstances.

4. The “Second Step up in Basis.” Due to the high estate exemptions, the tax planning focus has shifted from estate tax avoidance to capital gains tax avoidance. Assets that are community property in California will receive a step up in basis at the death of the first spouse, which allows the surviving spouse to sell the assets without capital gains tax liability. Another step up in basis will occur for the assets that are funded in the A Trust at the death of the surviving spouse, allowing the children to sell the A Trust assets without capital gains tax liability. Although the assets allocated to the B Trust will receive a step-up in tax basis upon the death of the first spouse, those B Trust assets will not receive another step-up in tax basis upon the death of the second spouse. Removal of the B Trust will allow all of the assets to receive a second step up in basis on the second death.

Here is an example of how the loss of the second step up in basis can hurt financially. John and Jane Davis set up an A/B Trust in 1993. They were California residents. They owned one home and some Microsoft stock. John died in 1996. After John died, Jane placed the home in A Trust, and the Microsoft stock valued at $100,000.00 (the first step-up in basis) in B Trust. At the time when Jane died in 2019, the Microsoft stock was worth $1,000,000.00 ($900,000.00 in appreciation and no second step-up in basis). Their entire estate will pass federal estate tax free because it was far below the single exemption of 11.4 million dollars at the time. Regrettably, because the stock was in B Trust when Jane died, the Davis children will owe approximately $225,000.00 in capital gains tax (both federal and state) on the sale of the stock (because of its low basis of $100,000.00). Had there been no A/B Trust or if the stock was allocated to an A Trust, the capital gains tax hit would have been avoided completely.

5. Portability. Portability refers to the ability of a surviving spouse to claim the deceased spouse’s unused estate tax exemption (the “DSUE amount”) and “bank it” for future use. Portability can simplify estate planning for married couples by eliminating the need for a B Trust. With portability a married couple can transfer $25.84 million federal estate tax free in 2023. Prior to the law change you needed to fund the B Trust in order to preserve the first to die’s exemption. Portability must be elected, it is not automatic. In order to preserve the DSUE amount the surviving spouse must file a federal estate tax return (Form 706).

Here are the pros of an A/B or A/B/C Trust:

1. Bloodline protection. The B Trust or the B and C Trusts are irrevocable. For example, if spouses have children from a previous relationship, and wish to limit a surviving spouse’s ability to change the trust beneficiaries, a B Trust or the B and C Trusts may be desirable. Although inconvenient for the surviving spouse, the restrictions and associated administration costs may well be worth the peace of mind knowing that the children will receive an inheritance.

2. Caregiver manipulation. You have all heard the stories about the manipulation by a caregiver later in life that results in an amendment of the estate plan that benefits the caregiver. Although there are laws in California designed to disqualify these types of gifts, an A/B Trust or A/B/C Trust will significantly limit the damage that can be done.

3. Late in life marriages. We have seen individuals get married with the new spouse promising “don’t worry, I will take care of your kids.” An A/B Trust or A/B/C Trust will prevent the surviving spouse from leaving everything to the new spouse.

4. Large estates. Couples with estates in excess of $25.84 million (the combined exemption of each spouse) should consider retaining the B Trust or the B and C Trust provisions to avoid the possibility of a 40% death tax owed upon the second spouse’s death.

5. Creditor protection. Because the B and C Trusts are irrevocable, they provide creditor protection. This can be significant for individuals in high risk professions such as doctors or general contractors. A surviving spouse can be sued and all of the A Trust assets can be lost to a creditor. But, the B and C Trust assets are protected from creditors and will be available for the surviving spouse and ultimately the children. Additionally, “spend thrift” provisions can be added to the B and C Trusts to protect the trust assets from the creditors of the children.

What should you do?

Review your trust now. You must weigh the pros and cons of using an A/B or A/B/C Trust planning and make the best choice for your personal circumstances. The overwhelming majority of our clients are converting their trust to a non-AB Trust by way of a trust restatement. We strongly recommend that most families whose assets are far below $12.92 million exemption create a non-AB Trust, or restate their current trust to a non-A/B format.

We highly encourage our clients, and potential clients, to review their existing trusts and contact us should they wish to discuss these important issues further. Many of our surviving spouse clients seriously regret not removing the A/B or A/B/C Trust provisions when they had the opportunity to do so. They are now forced to deal with a burdensome and costly trust administration. Do not let this happen to you and your family. The time to review your trust and act is now.

If you have any questions or would like more information, please don’t hesitate to call (877-585-1885), email us or register to one of our free workshops . We happily serve clients in California including Ventura County, San Luis Obispo County, Santa Barbara County, Los Angeles County, and Kern County.

By Christopher Botti, Esq., Certified Specialist in Estate Planning, Trust and Probate Law